3 Stocks to Buy Under $10 That Could Triple From Here

Savvy investors do not always chase expensive stocks to find high-growth opportunities. In fact, some of the most exciting plays in the market trade lower than $10, offering investors the chance to multiply their money over time if the underlying businesses deliver. Here are three stocks under $10 that Wall Street believes could potentially triple from current levels.

Penny Stock #1: Sana Biotechnology

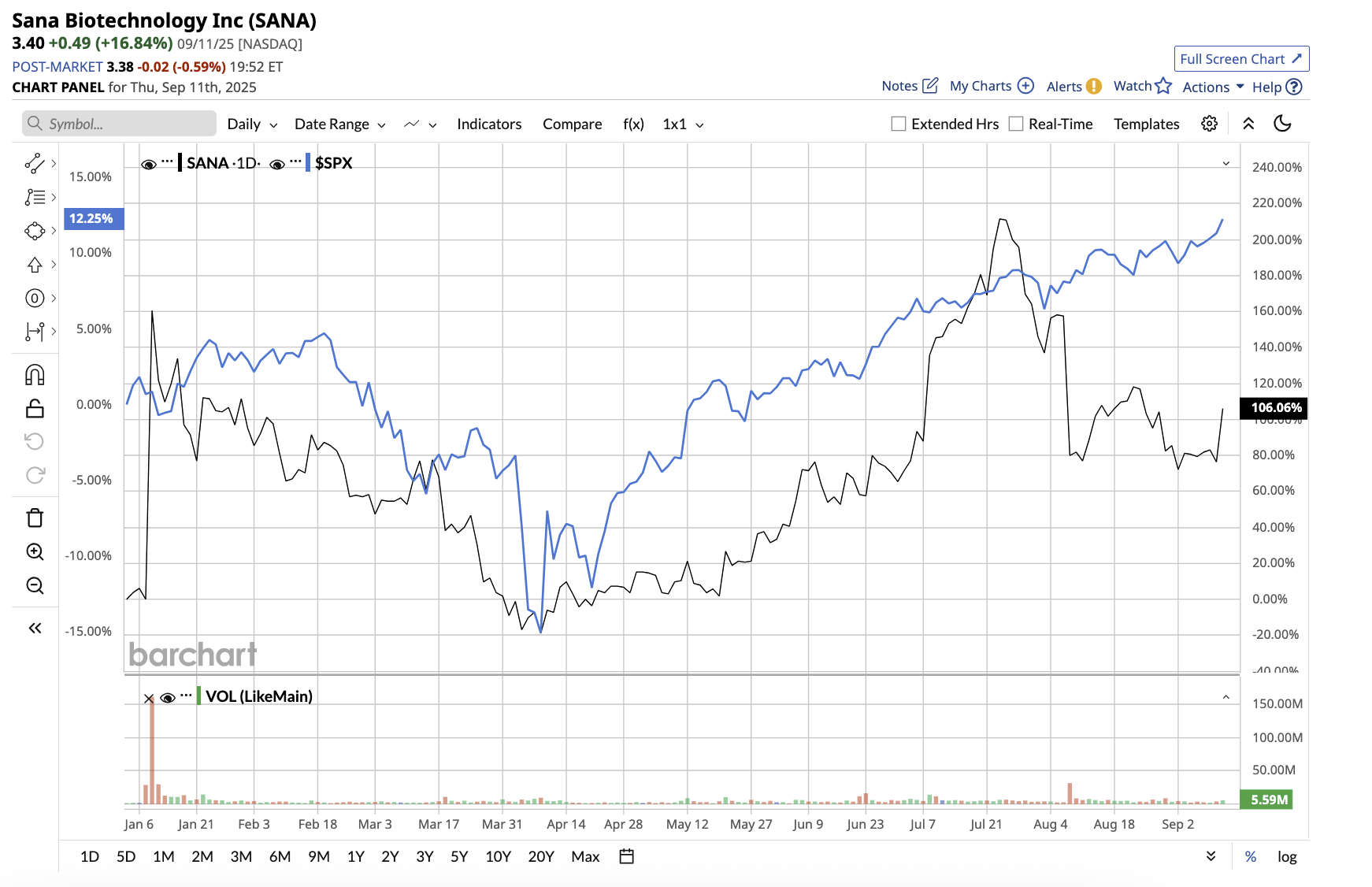

Valued at $837.6 million, Sana Biotechnology (SANA) is a biotech company that creates modified cells and gene therapies. Its goal is to repair or replace damaged cells, control gene expression, and make innovative medicines widely available to patients.

A breakthrough in its Type 1 diabetes research has propelled its stock up 100% year to date (YTD), with Wall Street believing it can yet triple from here.

In the second quarter, the company highlighted the ongoing success of Sana's UP421 trial, an investigator-sponsored research at Uppsala University Hospital that uses hypoimmune (HIP)-modified pancreatic islet cells to treat type 1 diabetes. Sana is anticipating offering a “broadly accessible single treatment with no immunosuppression leading to long-term normal blood glucose without exogenous insulin.”

Beyond diabetes, Sana is working on a variety of programs, including allogeneic CAR T therapies, specifically the SC291 (GLEAM trial) for B-cell-mediated autoimmune diseases like lupus and vasculitis, and the SC262 (VIVID trial) for relapsed/refractory B-cell malignancies in patients who have previously received CD19 CAR-T therapies. Both Phase 1 clinical trials are enrolling patients, with results expected by 2025.

Sana has also significantly expanded its financial runway by raising funds through an at-the-market sale and a public equity offering. It ended the second quarter with $72.7 million in cash, which increased to a pro forma $177.2 million after the capital raises. The company expects this to fund operations until the second half of 2026. Sana's breakthrough for diabetes is one of the most promising initiatives to date in developing a functional treatment that does not require lifelong immunosuppression. This could be a significant opportunity for Sana, presenting a high-risk, high-reward biotech investment.

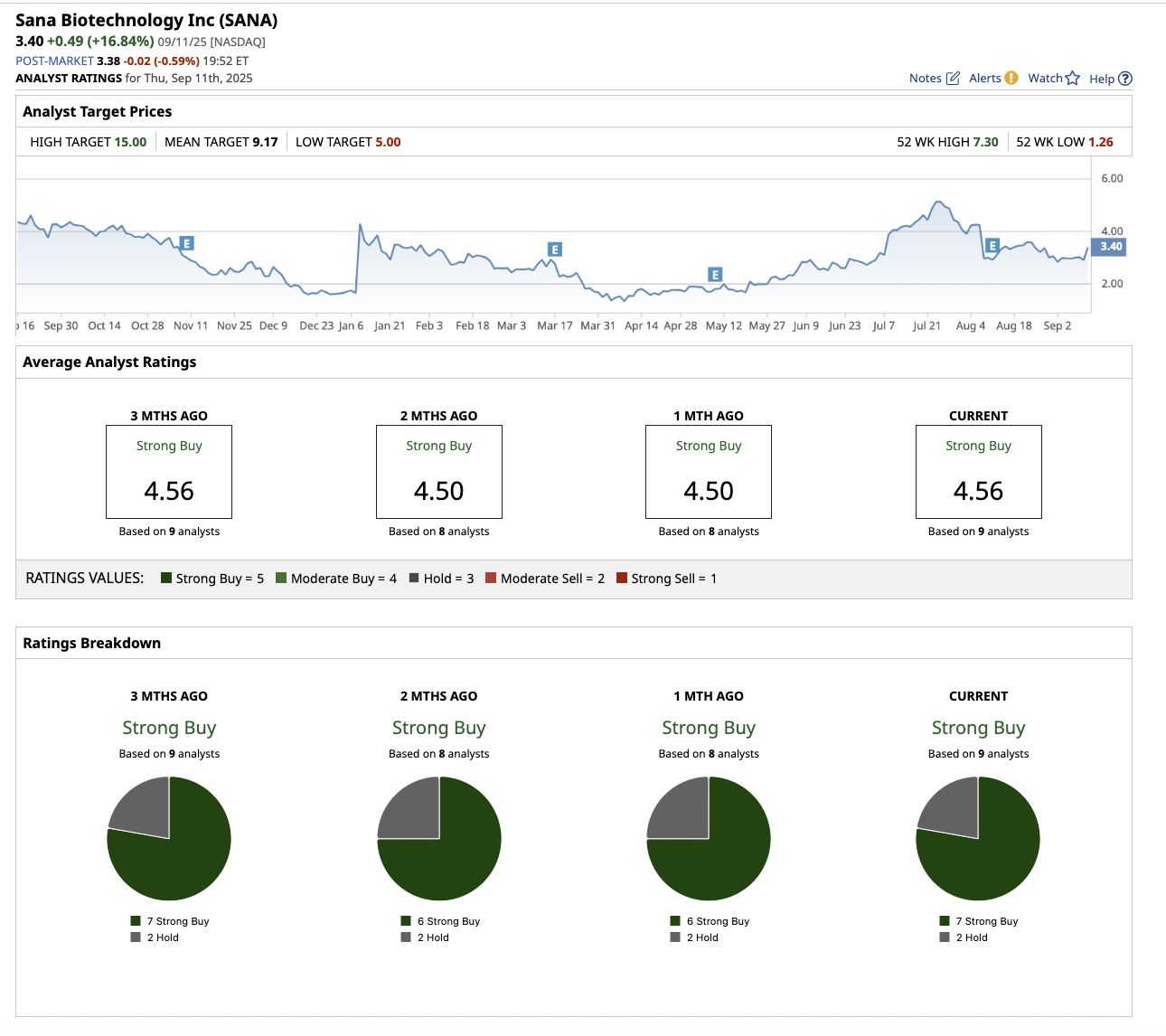

Overall, Wall Street rates SANA stock as a “Strong Buy.” Of the nine analysts who cover the stock, seven rate it a “Strong Buy,” and two suggest a “Hold.” Based on the average target price of $9.17, the stock has an upside potential of 169.7% from current levels. Its Street-high estimate of $15 further implies the stock can go as high as 341.2% in the next 12 months.

Penny Stock #2: Iovance Biotherapeutics

Valued at $875.7 million, Iovance Biotherapeutics (IOVA) is a commercial-stage biotech company that develops and markets tumor-infiltrating lymphocyte (TIL) therapies for the treatment of cancer.

Unlike many other cell therapies (such as CAR-T), which have mostly targeted blood cancers, Iovance's platform is intended to treat solid tumors like melanoma, lung cancer, and endometrial cancer.

While the stock is down 69% YTD, Wall Street expects the stock to soar around 700% above current levels based on its high price target.

Last year, the FDA approved Amtagvi (lifileucel) as the first and only T cell therapy for a solid tumor, specifically for patients with metastatic melanoma who have progressed despite traditional treatments. Amtagvi is now commercialized in the U.S. and is being reviewed for approval in other countries, including Canada, the U.K., and Australia. In the second quarter, overall product revenue of $60 million nearly doubled YoY. This growth was mostly driven by Amtagvi, which earned $54.1 million in revenue from treating 102 commercial patients in the U.S.

Proleukin, an interleukin-2 (IL-2) treatment that is commonly used as part of the Amtagvi regimen but is also supplied for other research and therapeutic applications, contributed an additional $5.9 million in sales. Iovance reiterated its full-year sales target of $250 million to $300 million, citing consistent growth in U.S. adoption and expected international expansion.

Beyond melanoma, Iovance is working on TIL therapy for non-small cell lung cancer (NSCLC), endometrial cancer, and frontline advanced melanoma.

Although revenue is increasing, Iovance has yet to show a profit. Net loss stood at $111.7 million in Q2. At the end of Q2, Iovance had $307.1 million in cash, equivalents, and investments. It also estimates $100 million in annual cost savings, which will allow the company to prolong its cash runway into the fourth quarter of 2026.

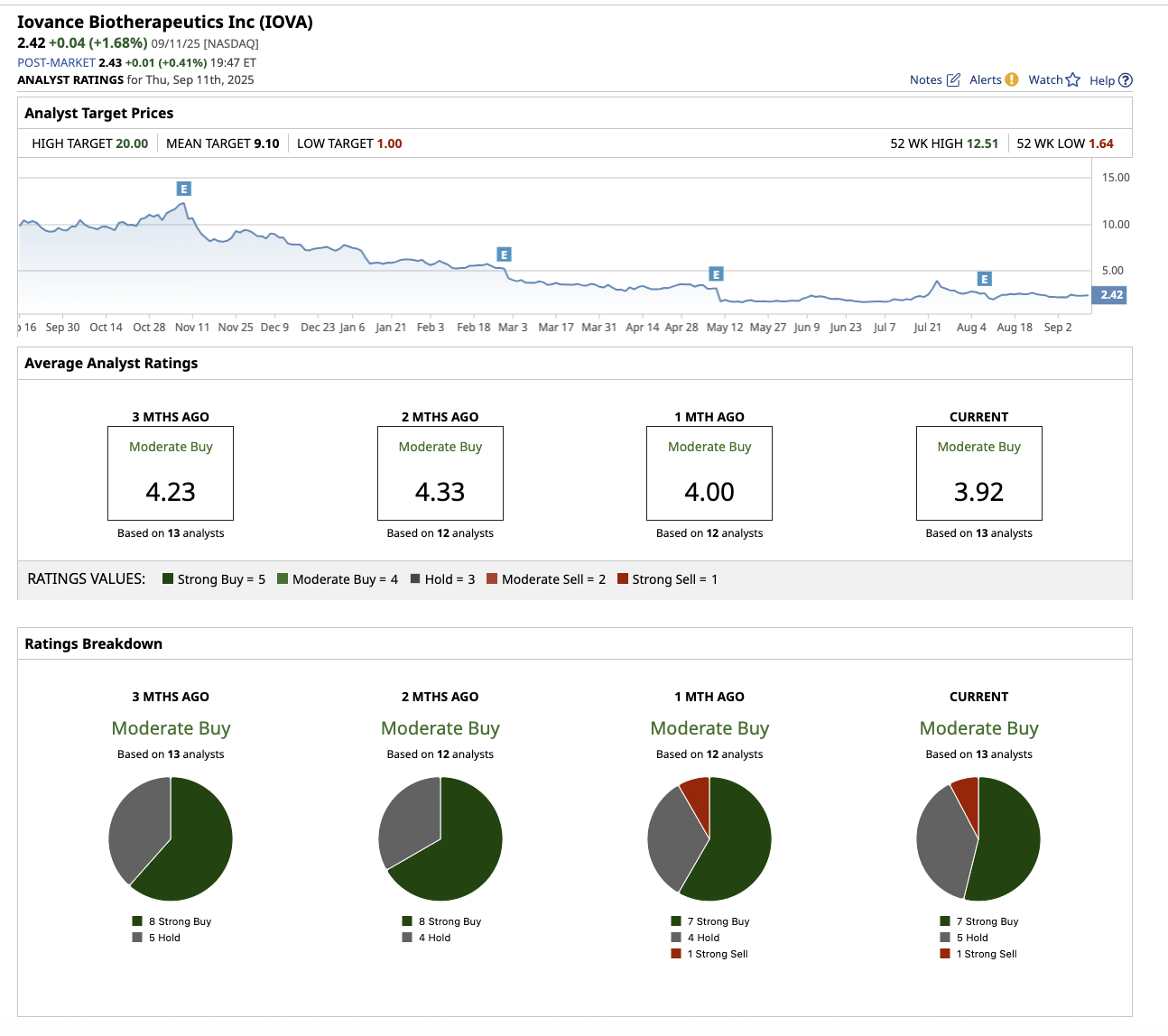

Overall, Wall Street rates IOVA stock as a “Moderate Buy.” Of the 13 analysts that cover the stock, seven rate it a “Strong Buy,” five suggest a “Hold,” and one suggests a “Strong Sell.” Based on the average target price of $9.10, the stock has an upside potential of 276% from current levels. Its Street-high estimate of $20 further implies the stock can go as high as 726.4% in the next 12 months.

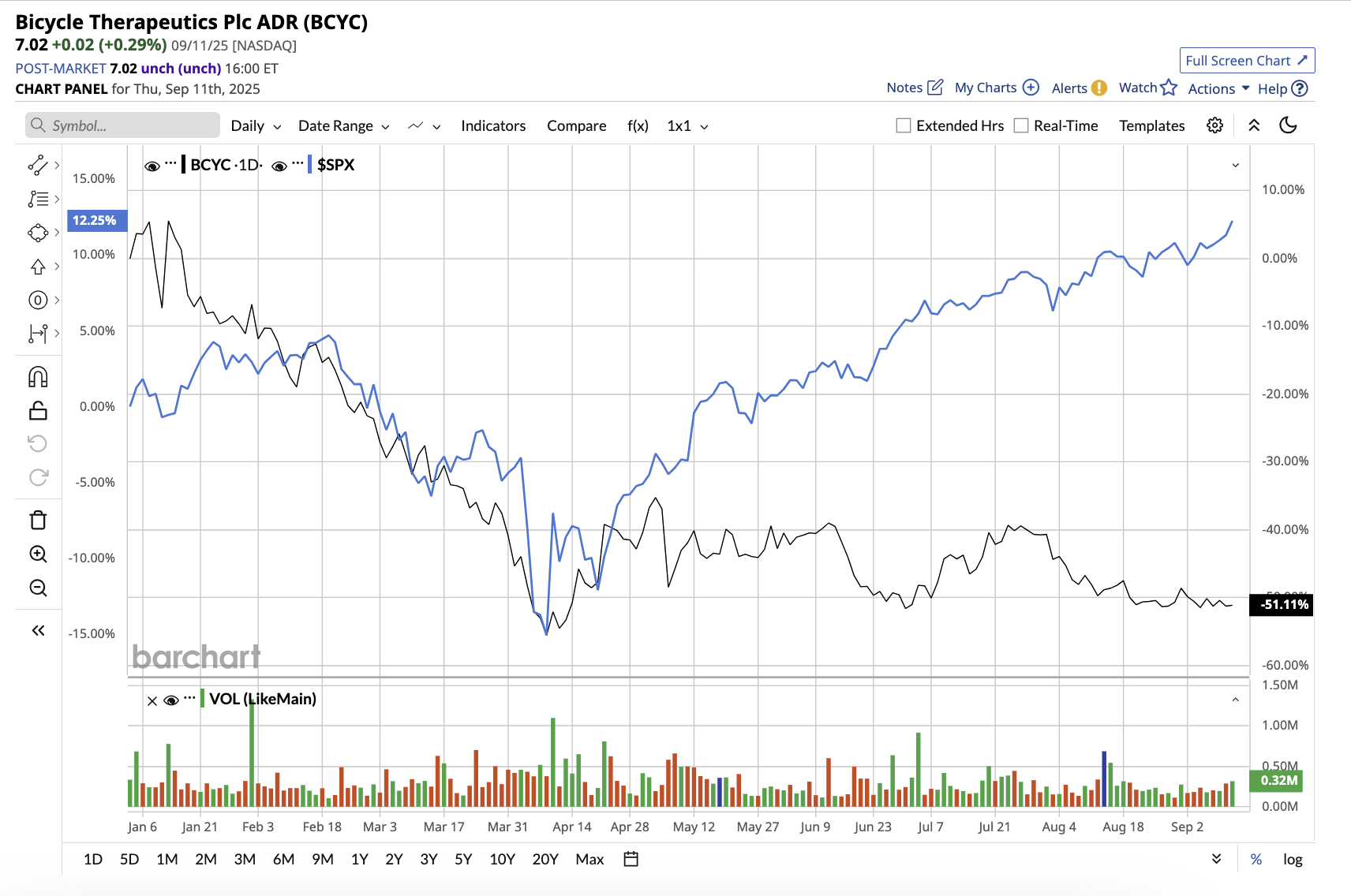

Penny Stock #3: Bicycle Therapeutics

Valued at $486.5 million, Bicycle Therapeutics (BCYC) is a clinical-stage pharmaceutical company creating a new class of medications using its proprietary Bicycle technology. While the company's primary emphasis is oncology (cancer therapies), the platform also has potential in other areas. This is why Wall Street expects the stock to skyrocket from here, despite a 51% drop YTD.

The company's methodology is based on bicycle molecules, which are synthetic short peptides (small amino acid chains) that are chemically bound into two loops, resulting in a bicyclic structure. Its lead program, zelenectide pevedotin, is a Bicycle Drug Conjugate (BDC) that targets Nectin-4, a well-validated tumor antigen. It is being tested in numerous Duravelo phase 1/2/3 trials for metastatic urothelial carcinoma (mUC), non-small cell lung cancer (NSCLC), and other solid tumors.

The company has no approved product yet. Hence, net loss widened to $79 million in the second quarter due to an increase in R&D expenses related to zelenectide pevedotin and other pipeline initiatives. At the end of Q2, Bicycle had cash and cash equivalents totaling $721.5 million. To improve its financial picture, Bicycle launched a 30% cost-cutting program, which included a workforce reduction. The company anticipates that this would extend its financial runway until 2028 and provide flexibility in navigating volatile market conditions.

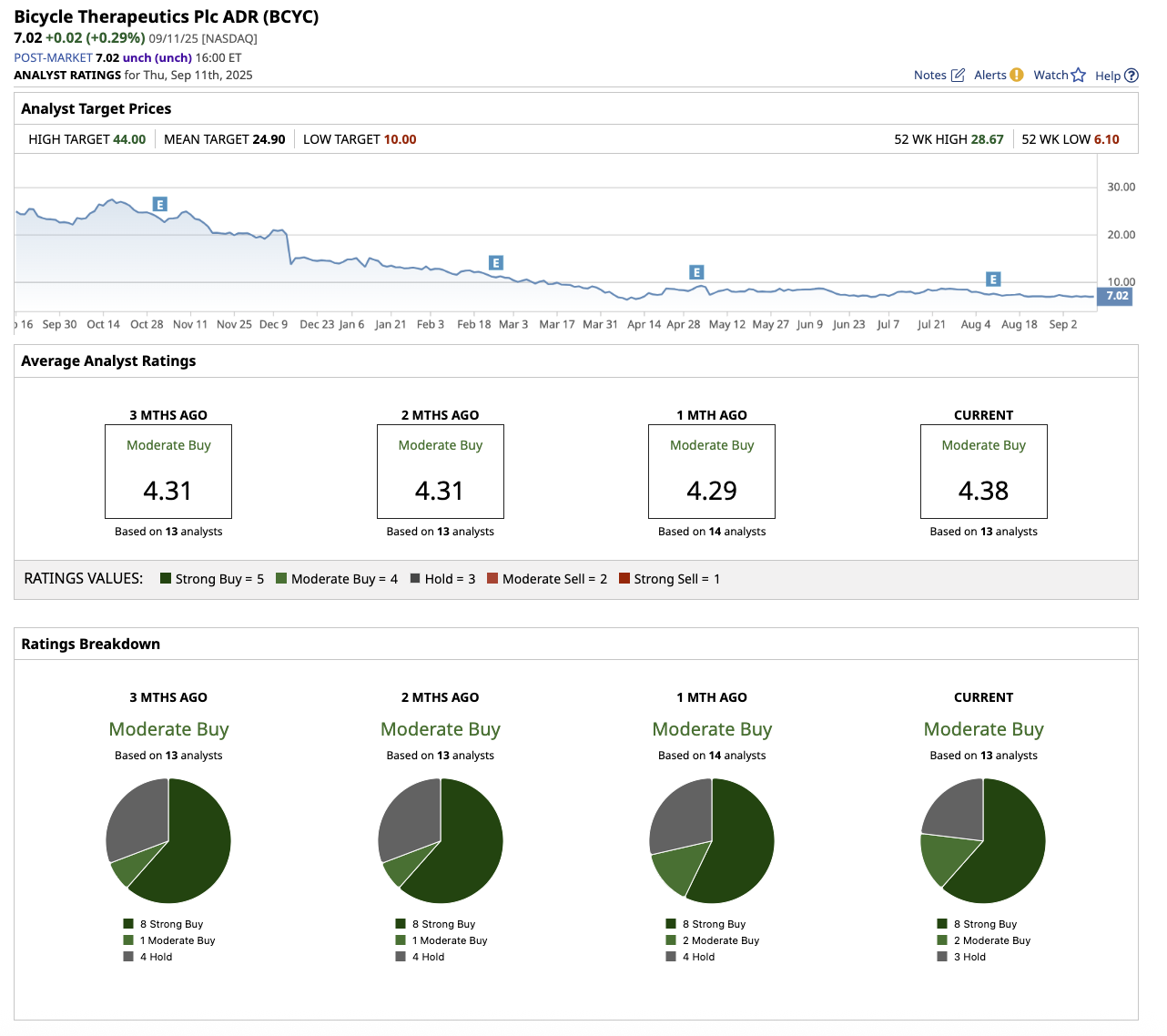

Overall, Wall Street rates BCYC stock as a “Moderate Buy.” Of the 13 analysts that cover the stock, eight rate it a “Strong Buy,” two say it is a “Moderate Buy,” and three suggest a “Hold.” Based on the average target price of $24.90, the stock has an upside potential of 254.7% from current levels. Its Street-high estimate of $44 further implies the stock can go as high as 526.7% in the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.